The Introduction of a New Technology, fulfilling its potential

This is the second in a two part article penned by 7 Layer staff. Read the first part here.

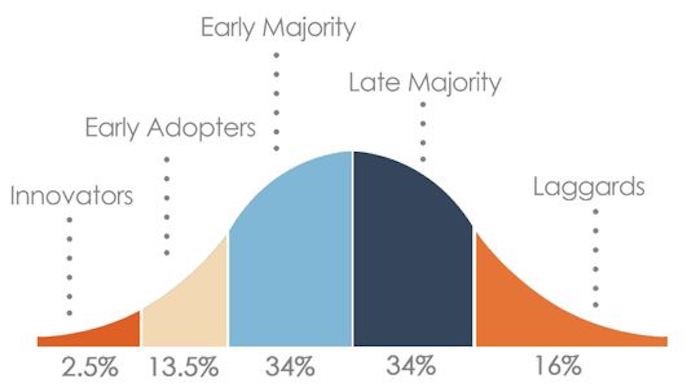

In the banknote industry the use of data analytics is moving through the “early adopter” phase of the innovation adoption curve [1]. This article speculates about what might be the full potential of great data combined with effective analysis at a time of changing cash usage.

Lessons from history

The benefits of adoption of a new technology are not achieved as a linear progression. A recent article by Jeff Funk in the Payments Journal looked at data from communication technology, starting with the telephone, with a lesson that is relevant for the changing cash cycle today.

In 1877 the leasing of telephone systems began in the USA. Until the patents of Bell Telephones expired in 1894, telephones were largely used by and within individual businesses. After the patent expired there was rapid growth in telephone systems and the number of users. This was led in cities by income groups who were not already using Bell systems, through mutual systems and, in rural areas, through what were known as “farmer lines”. Initially the telephone system providers were highly fragmented with small numbers of subscribers. As the number of businesses and subscribers increased, there was a consolidation in the number of telephone system providers which lowered costs, increased performance and allowed new services. In addition, the different telephone systems now worked as a single network. This move from working at a business level in 1894 to a whole networked community of users drove the growth that followed. By 1920 35% of US households had a telephone reflecting the immense value seen in them by their users.

This example shows that maximum value is released when technology is networked to be used widely. However, it is extremely rare for a new technology to move straight to being at a network level of operations. The costs are likely to be too high, the performance of the technology insufficient and it takes time for the evidence of value to be seen and accepted. The commercial benefit of enabling solutions to work together has to be agreed. As with the US telephone system, it is normal for new technology to start with a wide range of products and platforms and to operate within individual organisations. These small ecosystems use the technology based on immediate value around specific problems while building experience and demonstrating value with a series of success stories. This is where data analytics for banknotes is today.

In the long term, what could data analytics deliver for issue department?

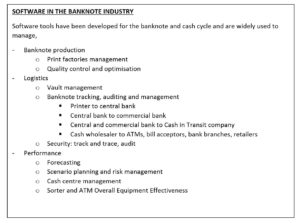

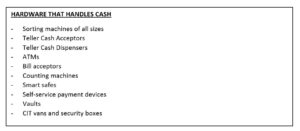

Improving the efficiency of the cash cycle is, in itself, a worthy goal. If cash is to become a minor payment tool, then the need to make it cost efficient at extremely low volumes, overcoming challenges of distribution and depositing, becomes vital. We believe great data will play a central role in achieving this. One view about how data analytics might develop is if organisations active in payments could draw data from all of the hardware and vaults used in the industry today (see box below), and their associated software tools. The Serial Number Interface Protocol (SNIP) initiative, which is being promoted by the Dutch National Bank, Bank of Israel and Bank of Canada, seeks to standardise the output of banknote handling equipment that reads serial numbers. This initiative is intended to deliver a common standard that will make data from banknote handling equipment of all kinds considerably easier to handle and work on than it is today. This will create the opportunity to have access to the broadest possible data sets, not just data from sorting machines. The cash management software used by CIT’s, commercial banks and ATM operators could provide data that would be useful for all parties to manage the cash cycle efficiently and effectively in ways not even considered to date. It could create the “network” benefits referred to in the telephone example. The size, quality, and detail of the data, in real time, would allow analysis to be done which is impossible today. Not all data will have serial numbers associated with it, but enough of the data will to allow serial number data to be used to understand cash flows, quality and performance in the entire cash cycle. If we knew how hard cash was working, we could manage the flow of banknotes to optimise their performance, reducing transportation costs and minimising stocks.

Just as the development of the telephone system moved forward rapidly once it was being used for more than highly localised purposes based on a highly fragmented variety of platforms, so we can expect to see the benefits of data analytics developing in the same way as adoption spreads. As cash usage changes, data analytics is likely to be at the heart of innovations to keep cash a vibrant payment tool. 7 Layer Solutions is working hard to deliver this new world recognising that, for now, we are still moving through the Early Adopter phase of innovation!

[1] See Currency News September 2019 article

By John Winchcombe, Currency Performance Consultant, 7 Layer Solutions

By John Winchcombe, Currency Performance Consultant, 7 Layer Solutions

First part printed in Currency News, September 2019 and also available here

Comments are closed.