Data Analytics – The Introduction of a New Technology

This is the first in a two part article penned by 7 Layer staff.

Data analytics is a new technology that is gaining acceptance and growing to fulfil its potential in the world of banknotes and the cash cycle. But what is it?

Central Banks have always collected and used data to model, forecast and manage their banknote needs. Until now this has been based on aggregated data of what has been issued, withdrawn, destroyed and put into stock. This data has largely come from vault management software and other ledger-based records.

Almost none of the data sources link back to individual banknote serial numbers. As a result, the ability to provide usable data about some key operational and policy topics is limited to using the averages inherent in aggregated data. Without that link to serial numbers, aggregated data cannot answer well questions about topics such as cash cycle velocity and flows, cash performance in circulation, quality levels, specification performance and optimisation, stock levels, forecasting etc. In addition, modelling based on aggregated data is only as good as the limitations that come with using averages as the starting point.

The ability to access information on banknote performance and the cash cycle based on high quality, high volume, detailed data down to the level of individual banknotes captured from the cash cycle is a new development allowing the full capability of data analytics to be used for the first time in Issue Departments. It is possible to achieve this due to four new developments:

- The use of Serial Number Reading (SNR) linked to sensor data. This is possible now due to the widespread use of optical cameras as part of the core technology platform in a very wide range of banknote handling equipment.

- The ability to connect to equipment to download data automatically, whether on site or remotely, is an everyday, low cost activity.

- The cost and complexity of data storage reducing significantly making it an everyday, low cost task.

- An increase in the number of people with data analytic skills and the development of tools means that the use of dedicated data analytic software is normal and an everyday part of business life.

Data analytics based on SNR data linked to sensor data offers the opportunity to do better.

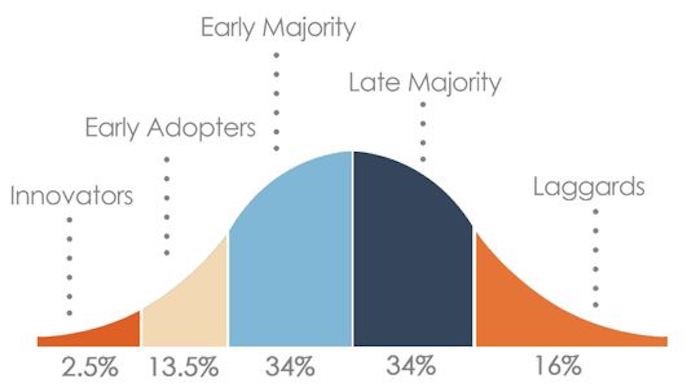

Where is data analytics in the innovation adoption lifecycle?

The four developments listed above have existed for a number of years. During this time a small group of central banks have been “Innovators” in this area, the Dutch National Bank, Bank of Canada, Bank of Israel, Bank of Lebanon and the South African Reserve Bank. These central banks and 7 Layer have been proving the technology and building case studies to demonstrate value. These banks created their own data analytic solutions. Their goals varied and their solutions have taken different technical approaches.

In addition, 7 Layer developed a data analytics product, NoteChain®, specifically for Issue Departments. Three central banks have shared their data with 7 Layer to be analysed by NoteChain®. As a result, 7 Layer now has the widest experience amongst this “Innovator” community. Another commercial provider has developed a software tool for use with print work data.

Significant experience has been gained about how to manage data and deliver the benefits efficiently and the technical challenges are now largely understood.

The use of banknote data analytics has now entered the “Early Adopter” stage where the technology is “de-risked” and evidence of the real value is being gained for use in business cases. The evidence for this is that,

- Other central banks are now collecting data and seven central banks over and above those mentioned already attend the 2018 International Banknote Analytics Seminar.

- Other commercial organisations are looking at developing software.

- The Dutch National Bank, Bank of Canada and Bank of Israel are leading an initiative called the Serial Number Interface Protocol (SNIP) which aims to standardise across all equipment that handles banknotes their data outputs. This will make the use of that data much easier to analyse and use. Standardisation has proved key in all other industries to allow new technology to gain scale and to improve performance.

- The Dutch, Canadian and Israeli central banks have all presented at conferences this year on the benefits they have gained from data analytics based on SNR data linked to sensor data.

What is the potential of data analytics as adoption grows?

There are a number of routes forward which would maximise the value from SNR.

- As the use of banknote data analytics moves through the different stages of the innovation adoption lifecycle, experience and knowledge is developing. Every central bank operates in a slightly different situation and this will help the technology become more useful and applicable. Standardisation of data formats and information sharing about how data analytics is being used will drive new innovation.

- At the moment, SNR with sensor data is limited to data down-loaded from sorting equipment used in sorting centres and print works. An important development will be to build experience of collecting data from sorters outside of the central bank (one central bank is now doing this). Given the move to decentralised sorting, this will allow much greater insights into the whole cash cycle.

- Being able to collect data from all types of banknote handling equipment remotely, including counters, bill acceptors, ATMs, teller cash recyclers etc.

Today data analytics is largely a central bank topic supported by companies such as 7 Layer. Already, learning is being shared and this will increase as it moves outside of central banks. Linkages across organisations and software platforms will allow a multiplier effect for the benefits. Given the fast-changing use of cash around the world, this may happen, and may need to happen, more quickly than we expect. The benefits should be significant and are likely to include those we have not yet even started to consider. Experience of other industries is that progress will accelerate from this point onwards. Time will tell!

By Phillip Ball, Development Director, 7 Layer Solutions

By Phillip Ball, Development Director, 7 Layer Solutions

As printed in Currency News, September 2019

Read part two here.