Making Better Business Decisions by John Winchcombe

Comment: John Winchcombe worked his way up to Product Manager and Marketing Director at De La Rue Currency over a fifteen year period and has been consulting with Phillip Ball, our Technical Director, to help promote our new note life cycle product, NoteChain.

Original article: Currency News, May 2016 edition (Link to Currency News issues)

In 2010 McKinsey published an article on the Internet of Things[1]. This argued that advances in technology allow organisations to collect an increasing volume and breadth of data in real time in order to make better decisions and even new decisions.

They categorised the benefits as either falling into “information and analysis” or “automation and control”. Have the benefits of these advances become a reality for Central Banks in the field of currency management?

Key Central Bank Decisons

The key banknote related decisions for any Central Bank are:

- How to understand the demand for banknotes and then manage their supply efficiently and cost effectively

- How to specify a banknote to achieve optimum performance in circulation for both note life and security against counterfeiting

Although high speed sorting equipment has been able to read serial numbers for many years (indeed the Dutch National Bank has done so since 1954), there has not been the data storage or computing power available to allow useful analysis. As a result, our industry has always struggled with getting reliable, useful and timely data to make these decisions.

The consequences of this can be painful. For example, “emergency” banknote printing orders due to failures of forecasting and stock management. These orders are fulfilled at premium prices. Or running a circulation trial to establish if, for example, a varnish will do what the supplier claims – a complex, laborious and expensive exercise.

Technology Benefits of Data

Today’s technology advances, however, mean that tracking individual banknotes and linking the output of all the fitness and authentication sensors is possible and cost effective.

There will never be a perfect picture of the cash cycle but this data, properly managed, could provide a Central Bank, each day, with

- Knowledge of what banknote stocks are where and how long they have been there

- How much life the banknotes have left in them before being unfit

- How the banknote is performing (how soiled, ink loss, tears, hologram damage etc)

If every machine in the entire cash cycle that had to fitness inspect a banknote could also read the serial number, with modern communication systems this data can be shared with the Central Bank. The benefits increase, of course, with every enabled and connected sensor.

Better data would allow the Central Bank and all members of the cash cycle to manage banknote stocks efficiently, to organise banknote printing orders and stock management, to avoid holding too many or too few banknotes, to maintain the desired level of clean banknotes and to specify the banknotes to address the actual causes of banknotes becoming unfit. There are mutual benefits for other wholesale cash users and this may encourage them to work with the Central Bank to extend the data collection network.

Clearly there is a one-off cost to put serial number reading on devices. There is also a software development cost, or licensing cost if bought in, and the cost of data storage and management. Relative to saving 5-10% per annum on the cost of buying, storing and managing banknotes and gaining control of note cleanliness, these costs are relatively small.

Who is doing what?

A number of Central Banks have started the journey of turning this into reality, particularly the Reserve Bank of Australia, the Bank of Canada, De Nederlandsche Bank and the Bank of Mexico with their Gogol project. They are writing the software required in-house which is not perhaps surprising given that they are at the leading edge of technology and thinking and all are large Central Banks.

Equally, until 7 Layer Solutions launched its “Note Life Cycle” product NoteChain this year, there has not been a commercial solution available written specifically to deliver these benefits for Central Banks. A number of organisations have talked about the concepts, and nearly all high speed sorter manufacturers, banknote equipment manufacturers, CIT companies and industry software companies have software solutions that deal with vault management or commercial cash management requirements (e.g. ATMs management).

First steps

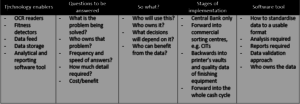

The first step is to define the scope of what is possible at what cost in what timescale. The starting point is the Central Bank’s own sorters and vault where it can easily obtain data feeds. Although most internal IT departments will be confident that they have the ability to run this project, the first task is to assess the presence or absence of key technology enablers, to consider exactly what questions need answering and how this will drive decision making. From this a quick cost/benefit analysis can be carried out. Based on this first look, the Central Bank can then decide whether to initiate a full project and start looking for partners, internal or external.

Summary

If we knew more about how banknotes circulate, why and when they become unfit, why would you not ask your supplier for an “in circulation performance guarantee”? In fact, why would you buy banknotes and not just “rent” them requiring the supplier to deliver the right number of banknotes in circulation at the right quality in the right place?

For now, this article lays out the new reality, that, with thought and planning, it is today possible to access accurate, relevant, timely data, analyse it and get key questions answered with all the benefit and value that that will bring.

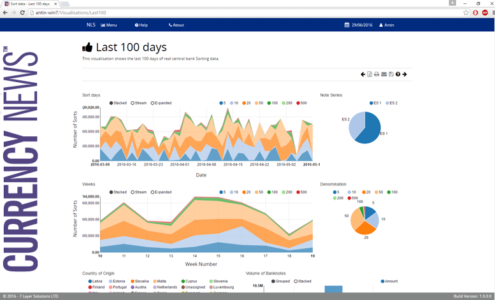

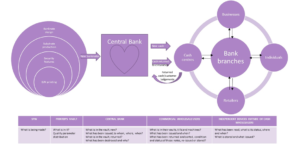

CASH CYCLE CHART WITH A TABLE CONSIDERING WHAT DATA COLLECTION IS NEEDED

DATA BENEFIT TABLE

Visual representation of the greater visibility in key areas with data feeds on fitness and authenticity.

[1] “The Internet of Things”. Michael Chui, Markus Loeffler, Roger Roberts

Comments are closed.